Most traders are familiar with delta and gamma. But there is another important driver of short-term flows in the S&P 500. Let’s go a bit deeper and examine the second-order Greeks: Charm and Vanna.

These two metrics don’t just explain options risk — they help forecast when and how market makers will move, and that flow is often what moves the market.

🧠 What Are Charm and Vanna?

Charm measures how much an option’s delta decays as time passes. —> ∂Δ/∂t

Vanna measures how delta shifts as implied volatility rises or falls. —> ∂Δ/∂σ

In simple terms:

Charm is time-driven: it tracks how hedging needs evolve as expiration approaches.

Vanna is volatility-driven: it shows how dealers must adjust hedges when volatility moves suddenly.

🔄 Why Should You Care?

Because market makers hedge their exposure using the underlying stock to stay neutral. This is called delta hedging and the goal is to maintain a zero delta exposure.

As charm decays delta over time, market makers adjust to stay balanced.

As vanna reacts to volatility, dealers adjust to hedge accordingly.

These flows cause predictable drifts and violent snaps — often unrelated to news or fundamentals.

🔁 Charm: The Scheduled Flow

Charm drives daily hedging adjustments as options decay. Think of it as a conveyor belt that steadily pushes prices.

Example:

A dealer is short puts (positive delta).

As time passes, the puts decay and their delta drops → the dealer’s position becomes over-hedged.

They must buy back stock to stay neutral.

🕒 Charm is predictable. It builds pressure slowly.

⚡ Vanna: The Event-Driven Flow

Vanna kicks in when implied volatility changes.

Example:

A dealer is short OTM puts or long OTM calls (both have positive vanna).

A vol spike increases the MM delta of those calls → the dealer must sell stock to stay neutral.

If vol drops, the MM’s delta decreases → they buy back stock.

The sign of net vanna tells you what market makers will do:

Positive net vanna + IV spike → sell stock

Negative net vanna + IV spike → buy stock (buying flows into rising volatility)

⚡ Vanna is reactive to changes in IV.

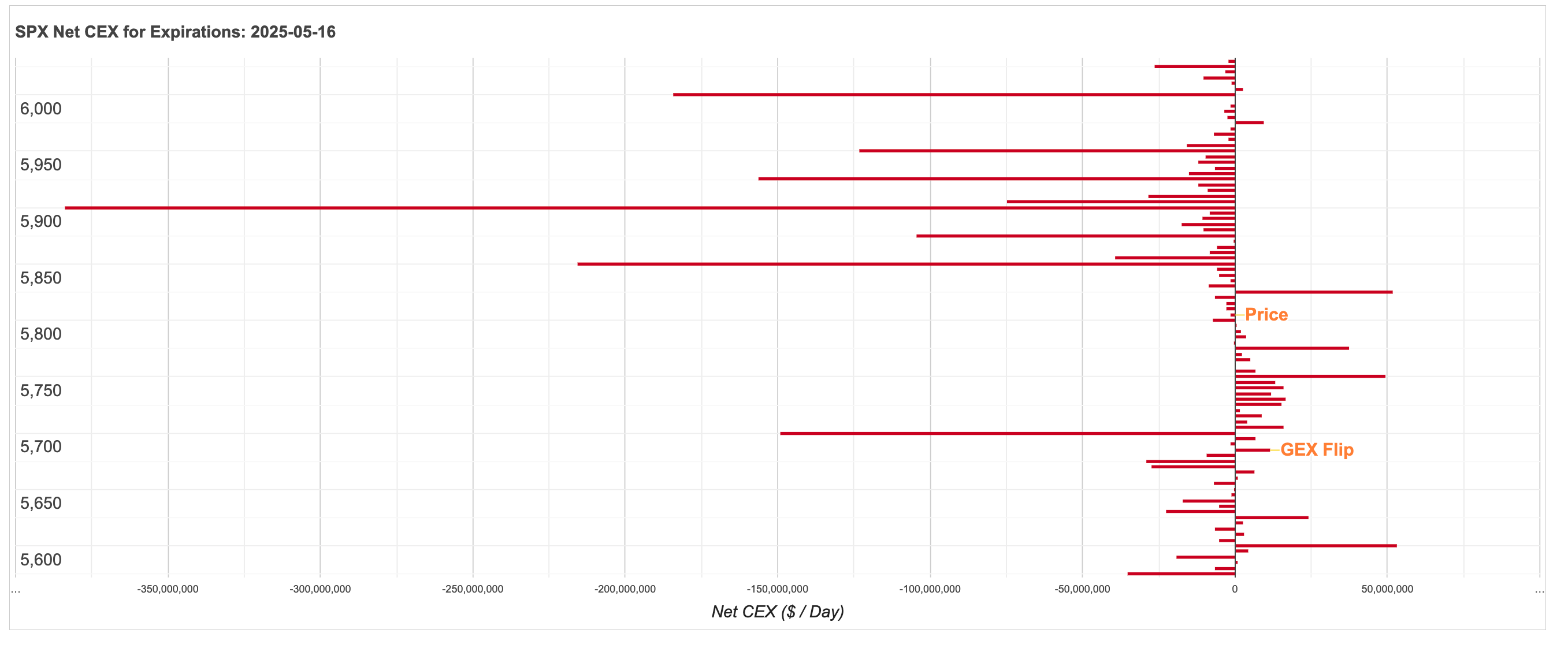

Real Example: SPX CEX

Charm is reported on the April 29, 2025 at -$597M for the 16May expiration

Market makers lose -$597 in delta per day. To stay neutral they must rebalance by buying the equivalent amount in shares.

Charm becomes more significant as days to expiration decreases, so this is more of an impact as an expiration date of significant open interest nears (monthly and quarterly opex).

🚨 Final Takeaway

Charm and Vanna explain dealer flows, and those flows often drive the market — especially around expiration and macro events.

Learn more at our Education Hub and see the data on our Charm & Vanna Charts page