Three strategies for trading volatility ETPs

Descriptions, weakness, and modifications to help you navigate VIX ETPs more intelligently

Here are 3 different strategies that are used to trade volatility ETPs (VXX, UVXY, SVXY, and TVIX). These strategies are all have long volatility ( $VXX ) and short volatility ( $SVIX ) components to benefit from cyclical increases and decreases in volatility.

Strategy 1: The VIX Futures Term Structure Strategy

This strategy is based on the term structure of VIX futures. The goal is to take advantage of a persistent roll yield and stay in the ETP that is in the same direction as the roll yield, e.g. SVIX when the term structure is in contango and VXX when the term structure is in backwardation.

You can measure this using a ratio of VX1 (first month VIX futures) to VX2 (second month VIX futures), VX1 to VX3, or spot VIX to VIX3M. It's all the same idea.

While a persistent contango can result is wonderful gains in SVIX, following this strategy as-is will generally have you underperform for a couple reasons.

Many people are watching the zero-line of the term structure (where VX1 = VX2). More often than not, equity support levels are at levels that coincide with a flat term structure. This is generally a better time to buy SVIX than to sell SVIX as the Term Structure trade strategy would suggest.

The near term VIX Futures contracts (front two months) rise together and fall together. The front two months can remain in contango and make daily gains over the course of weeks, which translates directly into losses for SVIX.

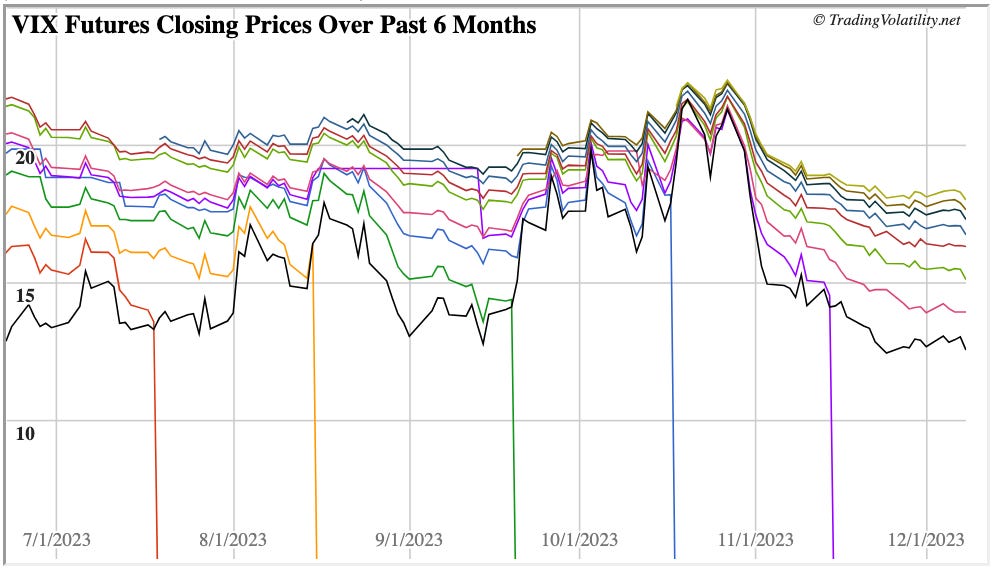

Below is a chart of the daily VIX and VIX Futures values over the past 6 months. Despite a persistent contango, there was a large increases through September ad October. However, if you monitor the spread between the lines to determine if that spread is getting narrower you’re going to hit the exit button before larger losses.

Modified Term Structure Strategy :

The key modification that needs to be incorporated when utilizing a Term Structure Strategy is to measure whether the spread between VX1 and VX2 is growing or shrinking. Rather than relying on a snapshot of the term structure, this allows you to also measure the direction and momentum of the front two months. This is an absolute must if you want to use a term structure strategy.

Strategy 2: The Volatility Risk Premium Strategy

The Volatility Risk Premium (VRP) is the difference between the implied volatility ( $VIX ) of $SPX and the realized volatility of $SPX.

The VRP is generally positive, meaning that implied volatility is higher than realized volatility since investors are usually willing to pay a premium over the levels of volatility that the market has experienced in the recent past (generally the past 5 to 20 days).

The idea here is that you short volatility when VRP is positive and buy volatility when VRP is negative. This is a very simple strategy that is maybe the most flawed and misguided for two primary reasons:

VIX is forward looking while realized volatility is backwards looking. In scenarios where the market is relatively calm but investors see risks ahead and want to buy protective puts, the VIX will rise and VRP has the potential to become more positive while SVIX falls.

Realized volatility is calculated by measuring how different the percent change in closing prices are over the course of a defined number of days.

A string of 5 days that has changes of +1%, +2%, -2%, +0.5%, -3% will have a high realized volatility and could help push VRP negative

string of 5 days that has change of -2%, -2%, -2%, -2%, -2% will have a realized volatility of 0 and will drive VRP higher. Meanwhile VIX is spiking and SVIX is plummeting.

After a VIX spike, the market resolves by going higher which often results in realized volatility moving even higher while VIX declines. This makes for a more negative VRP and enormous losses in a long vol trade while you wait weeks for VRP to go positive, because once again VIX is forward looking and Realized Vol is backwards looking, i.e mostly irrelevant.

Below is a graph of VIX vs realized volatility (also sometimes called Historical Volatility HV) which helps to visualize the above.

Modified VRP Strategy:

Include $VVIX (the volatility of $VIX) in the calculation of the VRP. Employing a measurement of where VVIX is trading relative to a short-term exponential moving average (EMA) is a great way to measure the direction and momentum of VIX.

When $VVIX is moving higher it means investors is expecting volatility to increase. This is when you want to close out your short volatility and buy volatility.

When $VVIX is declining, it means that the market is expecting volatility to be calm. This is a good time to sell volatility. This is a much better indicator of when to buy or sell volatility ETPs than the VRP alone.

Strategy 3: VIX Gamma Exposure Strategy

This strategy is based on the gamma exposure of VIX. What you're doing in actuality here is measuring sentiment on VIX via Open Interest of calls vs puts in VIX options strikes that are at currently near and at-the-money.

A prevalence of open interest in puts below the current price generally means that investors are selling VIX and selling calls. This is when we want to be long SVIX.

A prevalence of open interest in calls above the current price generally means that investors are buying VIX in preparation for a market decline. This usually only happens when a significant market decline is imminent or in-progress. This is where we see the exit signal for SVIX and buy for VXX.

In short, buy SVIX when the Skew-Adjusted Gamma Exposure is positive and buy VXX when the SA-GEX is negative.

Notes on long volatility ETPs (VXX, UVXY, SVXY, and TVIX):

Profiting from long volatility is a difficult task, primarily because volatility is mean reverting. This means that volatility spikes are generally short-lived and proceeded by a period of calm. Volatility spikes because some unknown event happens, which makes it impossible to predict. Buying volatility after the spike is often too late unless that events snowballs into a larger issue. Even if you do get into VXX early and ride a short trend higher, you're in a trade that can swing wildly on a daily basis and very often resolves by erasing all gains over the course of a few days.

We generally wait for all three of our indicators to signal a buy for VXX before being long VXX. If any of the indicators are not signaling a buy, we move out of VXX to prevent us from getting caught in a long vol trap.

A Final look on the modified versions of these strategies:

Red is the daily price of VXX. Blue is the indicator value where a negative is a signal to short VXX (or long SVIX) and a positive value is a signal to buy VXX.